Imagine you put $1,000 worth of ETH and DAI into a DeFi pool, hoping to earn trading fees. A week later, ETH spikes 50%. You check your balance - you have less than $1,000 in value, even though the market went up. That’s impermanent loss. It’s not a hack, not a scam. It’s math. And if you’re providing liquidity in DeFi, you need to understand it before you deposit a single coin.

How Impermanent Loss Actually Works

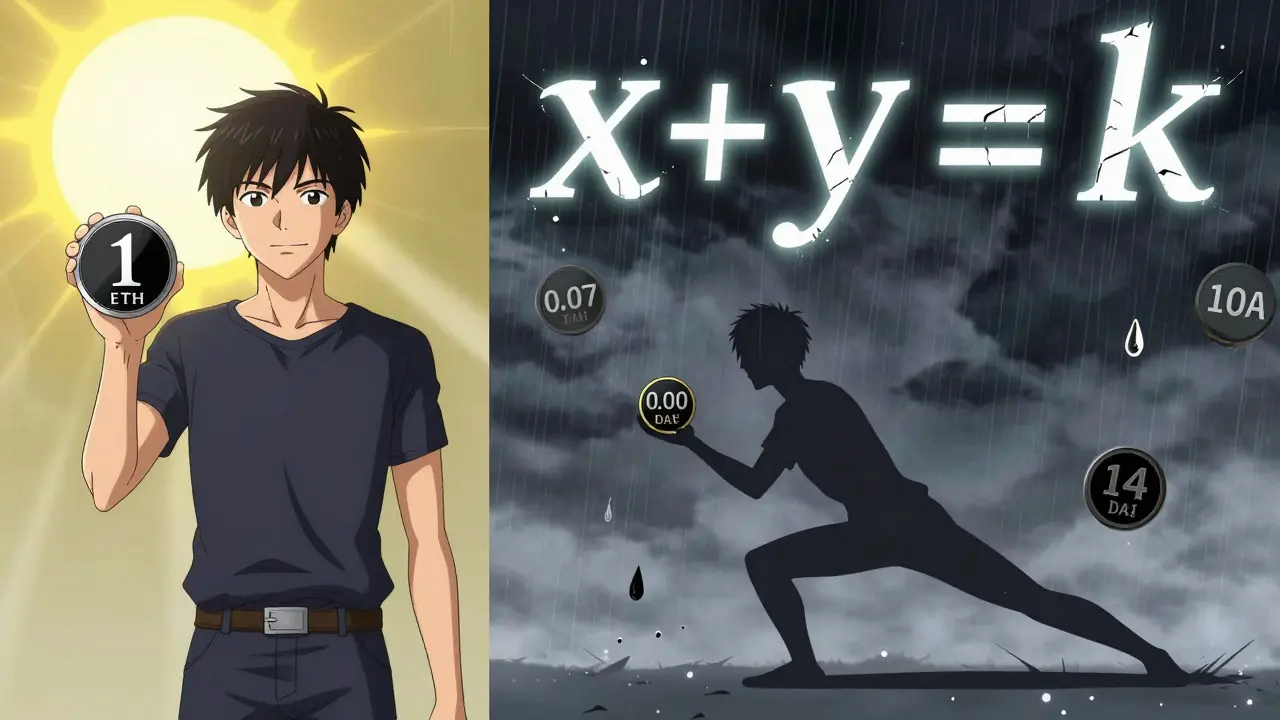

Impermanent loss happens when you provide liquidity to an automated market maker (AMM), like Uniswap, SushiSwap, or Balancer. These platforms don’t use order books like Coinbase or Binance. Instead, they use a formula: x * y = k. That means the product of the two assets in a pool always stays constant. When someone trades, the ratio of assets shifts to keep that formula true. Let’s say you deposit 1 ETH and 100 DAI into a pool. At that moment, ETH is $100, so your total deposit is $200. The pool now holds 1 ETH and 100 DAI. You own 10% of the pool, so your share is worth $20. Now ETH rises to $200. Traders start buying ETH from the pool using DAI. To keep the formula balanced, the pool gives away ETH and takes in DAI. By the time ETH hits $200, the pool might have 0.7 ETH and 140 DAI. Your 10% share? That’s 0.07 ETH and 14 DAI. At current prices, that’s $14 + $14 = $28. But if you’d just held your 1 ETH and 100 DAI outside the pool, you’d have $200 + $100 = $300. You didn’t lose money in fiat terms. You lost out on gains. That’s the core of impermanent loss: it’s an opportunity cost. The loss is only "impermanent" if the price goes back to where it started. If you withdraw now, it becomes real.Why It’s Worse Than You Think

Most people assume impermanent loss only happens when one asset crashes. But it’s just as bad - or worse - when one asset surges. The bigger the price swing, the bigger the loss. And it’s not linear. A 2x price change causes about a 5.7% loss. A 5x change? That’s over 25%. A 10x move? You’re looking at nearly 40% loss. Here’s the brutal part: even if both assets go up, you can still lose. Say ETH goes from $100 to $200, and DAI goes from $1 to $1.10. You’d think you’re ahead. But because ETH moved so much faster, the pool rebalanced, and you ended up with less ETH than you’d have if you just held. The math doesn’t care about your feelings. It cares about ratios. This is why liquidity providers in volatile pairs like ETH/SHIB or BTC/ALT often get burned during bull runs. The altcoin rockets, the pool gives away too much of it, and you’re left holding a pile of tokens that didn’t appreciate as much.When Impermanent Loss Is Minimal - or Even Helpful

Not all liquidity pools are created equal. Stablecoin pairs like USDC/USDT or DAI/USDC rarely see price changes. That means the ratio stays almost perfect. Impermanent loss here is near zero. That’s why many beginners start here. You earn trading fees - often 0.01% to 0.1% per trade - without worrying about losing value. Even better, some pools like Curve Finance are designed specifically for stablecoins. They use different algorithms that minimize slippage and reduce impermanent loss even further. These pools are popular with users who want steady, low-risk income. There’s also a twist: if you’re providing liquidity to a pair where one asset is your own token (like a new DeFi project), and you believe it will rise, impermanent loss might be worth it. You’re not just earning fees - you’re getting exposure to a token you think will go up. Some DeFi users treat liquidity provision as a way to accumulate assets over time, betting that the fees and rewards will outweigh the loss.

How to Protect Yourself

You can’t eliminate impermanent loss. But you can manage it. 1. Stick to stable pairs if you’re risk-averse. USDC/DAI, USDT/USDC - these are the safest. You won’t get wild returns, but you won’t get wiped out either. 2. Only provide liquidity if fees + rewards beat the expected loss. If ETH/DAI has 0.5% daily fees and you expect a 20% price swing, run the numbers. Most calculators show you need at least 10-15% in fees just to break even after a 2x move. 3. Use Uniswap V3 - concentrated liquidity. Unlike older versions where your money is spread across all price ranges, V3 lets you set a custom price range. If you think ETH will stay between $180 and $220, you can lock your liquidity there. You earn way more fees in that range, and if the price moves outside, your position becomes inactive - no loss, no gain. It’s like having a stop-loss built in. 4. Don’t chase yield without understanding risk. Pools offering 50% APY? That’s usually a red flag. High rewards often mean high volatility. You’re being paid to take on risk. Make sure you know what that risk is. 5. Track your position. Use tools like DeFi Saver, Zapper, or even Uniswap’s own analytics. Watch how your share value changes compared to just holding. If you’re losing more than 5% over a month, reconsider.What Happens When You Withdraw

When you pull your liquidity out, the loss becomes permanent. The protocol returns your assets based on the current ratio in the pool. If ETH is up 3x and you’re down 20%, you’re not getting your original 1 ETH back - you’re getting less. And that’s it. No going back. Some users wait for prices to recover before withdrawing. But that’s gambling. Markets don’t always return to old levels. A coin that crashes 80% might never come back. If you’re not sure, it’s better to cut losses early than hold onto hope.

Is Impermanent Loss a Dealbreaker?

No. But it’s a reality. DeFi didn’t invent loss - it just made it visible. On centralized exchanges, you don’t see it because you’re not providing liquidity. You’re just trading. In DeFi, you’re part of the market engine. And engines wear down. Many successful liquidity providers treat it like a business. They diversify across stablecoin and volatile pools. They reinvest fees. They monitor prices daily. They know that for every 10% loss on a volatile pair, they might make 15% in fees over six months. The key is awareness. If you understand the math, you can make smart choices. If you don’t, you’re just guessing - and guessing in DeFi usually costs money.Bottom Line

Impermanent loss isn’t a bug - it’s a feature of how AMMs work. It’s the price of decentralization. You give up control over your asset ratio to let the market trade automatically. In return, you get fees and sometimes rewards. But if you don’t know how it works, you’re not a liquidity provider. You’re a lottery ticket buyer. Start small. Use stablecoin pools. Learn the tools. Watch your positions. Only move into volatile pairs when you’ve got a clear reason - and a plan to handle the math. Because in DeFi, the biggest risk isn’t hackers. It’s not knowing what you’re really signing up for.Is impermanent loss real money loss?

It’s not a loss in fiat terms unless you withdraw. It’s an opportunity cost - you miss out on gains you’d have had by holding the assets outside the pool. But if you pull your liquidity out after prices shift, the loss becomes real and permanent.

Does impermanent loss happen on centralized exchanges?

No. Centralized exchanges use order books, not automated market makers. When you trade on Binance or Coinbase, you’re buying or selling directly to another user. You don’t provide liquidity, so you don’t face impermanent loss.

Can you avoid impermanent loss entirely?

Not completely, but you can minimize it. Use stablecoin pairs like USDC/USDT, stick to low-volatility assets, or use Uniswap V3’s concentrated liquidity feature to limit your exposure to specific price ranges. Avoid high-risk pairs unless you fully understand the math.

Why do people still provide liquidity if there’s impermanent loss?

Because they earn trading fees - often 0.1% to 1% per trade - and sometimes bonus token rewards. In stablecoin pools, fees can outweigh minimal impermanent loss. In volatile pools, some users bet that the rewards will cover losses over time. For many, it’s a way to earn passive income while holding crypto.

What’s the difference between impermanent loss and slippage?

Slippage is the difference between the expected price of a trade and the actual price you get - it happens when you trade on a small pool. Impermanent loss is what you, as a liquidity provider, lose because the pool’s asset ratio changed due to trades. Slippage affects traders. Impermanent loss affects providers.

Do I need to pay gas fees to withdraw liquidity?

Yes. Removing liquidity requires a transaction on the blockchain, which costs gas. On Ethereum, this can range from $10 to $100 depending on network congestion. Always factor gas into your profit calculations - it can eat into small gains, especially in stablecoin pools.

Is impermanent loss the same as a negative return?

Not exactly. A negative return means you lost money in USD terms. Impermanent loss means you made less than you would have if you’d just held your assets. You could still be up in USD - just not as much as you could’ve been.

Can insurance cover impermanent loss?

A few protocols like Nexus Mutual and Cover Protocol offer impermanent loss insurance, but they’re expensive, complex, and rarely used. Most users avoid them because premiums often cost more than the expected loss. It’s not a reliable solution yet.

Kip Metcalf

January 7, 2026 AT 05:42Man, I just dipped my toes in ETH/DAI and got wrecked when ETH went up. Thought I was winning till I checked the math. Turns out I was just holding a bag of DAI while the world moved on.

Natalie Kershaw

January 7, 2026 AT 20:12Y’all keep acting like impermanent loss is some secret trap. Nah. It’s just the cost of doing DeFi business. If you’re not earning more in fees than you’re losing on the spread, you’re doing it wrong. Start with stable pools, learn the curves, then go wild. No shame in being slow.

Mujibur Rahman

January 8, 2026 AT 12:07Impermanent loss isn't even the real issue here. The real problem is people treating AMMs like ATMs. You think you're earning yield but you're actually subsidizing traders. Every time someone swaps ETH for DAI on Uniswap, you're the one giving up your ETH at a discount. The protocol doesn't care. The traders don't care. Only you care. And you're the one getting cooked.

Mollie Williams

January 9, 2026 AT 10:07It’s funny how we call it 'impermanent' loss like it’s a consolation prize. Like the universe winks and says, 'Hey, it’s not really gone, just... temporarily misplaced.' But if the price never returns? Then it’s just loss with a fancy name. We’re not just doing math-we’re betting on the elasticity of markets, on human greed, on the hope that what goes up will eventually come back down. And sometimes? It doesn’t. That’s the quiet horror of DeFi. Not the hacks. Not the rug pulls. Just the slow, silent erosion of opportunity.

Surendra Chopde

January 11, 2026 AT 03:24First time I tried liquidity mining I lost 30% on a SOL/USDC pool. Learned my lesson. Now I only do stable pairs. Fees are low but at least I sleep at night. No drama, no panic checks. Just chill earnings.

Tre Smith

January 13, 2026 AT 02:42Most people don't even understand what a constant product market maker is. They see 20% APY and throw money in. Then they cry when they lose 15% to impermanent loss. That’s not DeFi’s fault. That’s your fault. You didn’t do the math. You didn’t read the docs. You didn’t even Google it. You just saw ‘yield’ and clicked ‘deposit’. Welcome to the zoo.

Rahul Sharma

January 13, 2026 AT 22:43Respected sir, impermanent loss is unavoidable in automated market maker systems. However, one may mitigate such risk by employing stablecoin pairs and utilizing concentrated liquidity mechanisms. Also, gas fees must be accounted for in net profit calculations. Thank you for your attention.

Don Grissett

January 14, 2026 AT 14:37yo i just got back from a 3 day trip and checked my uni v3 position. i had 1.2 eth and 1200 usdc. now i got 0.9 eth and 1400 usdc. i thought i was rich but turns out i lost 20% on eth. why does this happen??

Katrina Recto

January 15, 2026 AT 12:24Impermanent loss is just the market reminding you you’re not in control anymore. You gave up your asset ratio to let bots trade for you. Now you’re just watching the numbers bleed. No drama. No panic. Just math. And math doesn’t care if you believed in the coin.

Veronica Mead

January 16, 2026 AT 23:02It is imperative that individuals engaged in liquidity provision comprehend the inherent structural disadvantages of automated market makers. The mathematical underpinnings of the x*y=k model are not subject to sentiment, nor are they mitigated by optimism. One must approach this endeavor with the rigor of a quantitative analyst, not a hopeful retail participant.

Jessie X

January 18, 2026 AT 10:09Just started with USDC/DAI. No drama. No stress. Just slow steady fees. I’m not trying to get rich. I’m trying to not lose. And so far? Winning.

Tracey Grammer-Porter

January 20, 2026 AT 09:49if you’re new to this just stick to stable pairs. seriously. you don’t need to chase 50% apy on some random token pair. you just need to learn how the system works. i started with usdc/usdt and now i understand why my eth/daI position lost value. it’s not magic. it’s just math. and math is kinda beautiful when you get it.

Ritu Singh

January 20, 2026 AT 16:22They don’t want you to know this but impermanent loss is a stealth tax. The whole DeFi system is designed to transfer wealth from liquidity providers to traders and whales. You think you’re earning yield? You’re just the fuel. The protocol? It’s a Ponzi with a whitepaper. And the more you ‘earn’, the more you’re being drained. Wake up.

Gideon Kavali

January 22, 2026 AT 06:10Impermanent loss? That’s just the price of decentralization. America built the internet. We built DeFi. And now we’re paying the cost of freedom. Every time you provide liquidity, you’re not just giving up assets-you’re defending the open financial system. So yes, you lose a little. But you’re part of something bigger. And that matters.

Allen Dometita

January 23, 2026 AT 18:13bro i used to be scared of impermanent loss till i realized: if i’m earning 0.8% daily in fees on a stable pair, i’m making back my losses in like 3 weeks. now i just let it ride. the math works. trust the process 🚀

greg greg

January 24, 2026 AT 02:02Let me break this down because I’ve spent the last 72 hours reading whitepapers, running simulations in Python, and talking to five different DeFi yield farmers. The key insight isn’t that impermanent loss is bad-it’s that it’s asymmetric. When the price of one asset doubles, your exposure to that asset is halved, not because you sold it, but because the AMM rebalanced it for you. And here’s the kicker: the loss isn’t linear. It’s quadratic. So a 3x move isn’t 1.5x the loss-it’s roughly 4x. And if you’re in a volatile pair with high slippage and low volume? You’re not just losing to impermanent loss-you’re losing to bad design, bad timing, and bad assumptions. Most people don’t realize that the only time you truly benefit from liquidity provision is when both assets move slowly in the same direction. Otherwise, you’re just the liquidity sponge that soaks up volatility and gives nothing back. And that’s why the smart money goes to stablecoins or concentrated liquidity. Because they’re not trying to beat the market-they’re trying to survive it.

LeeAnn Herker

January 24, 2026 AT 18:29Wait… so you’re telling me the whole ‘decentralized finance’ thing is just a way to make rich traders richer by making small investors lose money while pretending it’s ‘fair’? And we call this innovation? Wow. I’m so glad I didn’t fall for this. Next they’ll say crypto is ‘financial freedom’ and I’ll be like… nope. I’ll just keep my cash under the mattress. At least there’s no algorithm stealing my gains.

Jennah Grant

January 25, 2026 AT 11:54Just wanted to say: if you’re new and scared of impermanent loss, start with Curve. Their stablecoin pools are engineered to minimize it. I’ve been in USDC/DAI/USDT for 6 months. Lost 0.8% total. Earned 12% in fees. That’s the sweet spot. No drama. Just steady. You don’t need to chase moonshots to win in DeFi.